Key Takeaways:

- Credit ratings can assess the financial stability of businesses and countries, while credit scores can assess the financial creditworthiness of individuals.

- Credit ratings are expressed in letters, while credit scores are represented by numerals.

- Knowing the distinction between credit rating and credit score is important for making good financial decisions and planning finances.

In the field of personal finance, two terms frequently pop up: credit score and credit rating. However, they both complement each other in identifying financial fitness, but they serve various purposes and address distinct entities. Let us dive deep into the concepts, explore the differences, and finally try to understand the role of these concepts in the financial landscape.

Credit Rating:

The credit rating, from the view of businesses and governments, serves as a basis of judgment for investors who seek creditworthiness. Represented in letter grades by prestigious companies like S&P Global and Moody’s, these stand as the ratings from AAA for those entities with the strongest financial capacity to D, meaning default.

Considered factors include past borrowings, payment discipline, cash flow, and borrowing levels. The ratings derive stability from a steady income and favorable economic environment, which translate into low risk for investments. S&P Global, Fitch Ratings, and Moody´s are among the agencies that expertly audit the paying-back credibility of the entity financed.

They analyze if there is any instance of a late or unpaid bill, bankrupt paper, or default, and access cash flows. These evaluations provide investors with essential information about the financial soundness and security of business organizations and governments.

Credit Score:

An individual’s creditworthiness is reflected in a three-digit number called a credit score. It falls within the 300–850 range and connected to an individual’s creditworthiness.

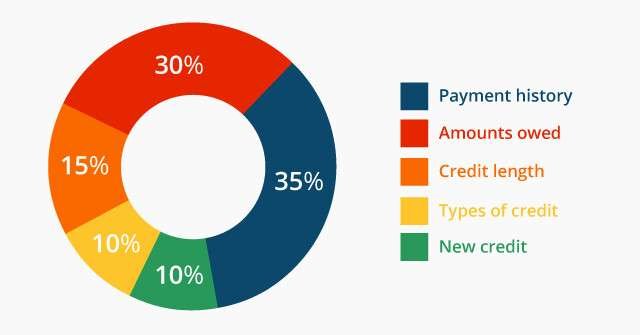

The FICO score is the most commonly used of all the scoring models. This model takes into account payment history, credit utilization ratio, length of credit history, and credit mix. A credit score for each individual is based on his or her payment history, credit mix, new credit accounts, and length of credit history. A higher score implies that an individual has a responsible credit management history. As a result, this helps a lender see the general creditworthiness of an individual and whether he or she is a responsible credit user.

Difference between Credit Rating and Credit Score:

Credit rating and credit score are two distinct metrics used to assess creditworthiness, but they serve different purposes and audiences.

Credit ratings apply to businesses and countries, and they help investors make decisions, while financial institutions use credit scores designed for households to inform their lending decisions.

It evaluate the financial health of an entity and its ability to sustain its financial obligations over the long term. The assigned ratings are essential for investors who are trying to decide whether to buy corporate or government debt securities.

However, the credit score is the source of information for the lenders, which helps them identify whether the individual is creditworthy or not. It also helps in assessing the risk attached to lending money to that individual.

The purpose of credit ratings is to evaluate the financial position of companies, while credit scores have the purpose of assessing the creditworthiness of individuals.

A three-digit number represents the credit score, whereas letters are used as a rating. Besides this, credit rating agencies use CRA, or credit rating, to assess an individual. The algorithms used to calculate credit scores focus on analyzing individual credit behavior.

Factors Influencing Credit Rating and Credit Score:

Multiple important factors affect both credit rating and credit score calculation, helping to estimate the creditworthiness of an entity. Payment history is of critical importance because the presence of timely payments has positive effects on both metrics. Whereas a late payment or filing bankruptcy can lead to a lower credit score and a damaged credit rating.

A significant factor in the calculation is the credit utilization ratio. It represents the fraction of credit being used out of the available amount. Keeping a low ratio will help us to still have a good credit standing and rating. Besides, the duration of the credit history shows stability, and the greater the stability, the higher the credit score.

More diversity in credit accounts, meanwhile, is also a positive contribution. A recent credit inquiry may temporarily lower your scores, whereas two negative public records, such as bankruptcy, can be very damaging. Periodic scrutiny of credit reports and prompt resolution of mistakes is an important step towards having 100% accurate information. It is an essential aspect of good ratings and scores.

Credit Rating & Score Impact on Financial Well-Being:

A credit score is a very important parameter that determines credibility and influences different aspects of personal finances. It gives a person access to credit, credit card interest rates, employment, housing, and general financial stability.

A robust credit rating and high credit score make credit acquisition possible on favorable terms, credit cards, and other forms of credit with lower interest rates and higher credit limits.

However, those who have poor credit ratings or scores might face problems getting credit. They might get a bad deal with high interest rates or stringent payment terms.

A positive credit history and a high credit score may improve your chances of getting your rental application approved. It will affect the rental conditions, such as the security deposit.

Likewise, mortgage lenders apply these ratings and scores as the basis for their evaluation of loan applications and interest rates.

All in all, maintaining a good standing with respect to the credit rating and a high credit score is critical for financial soundness and peace of mind. These metrics empower people to set their financial targets, take credit when appropriate, and make informed decisions relating to their finances.

Conclusion:

Determining the differences between credit rating and credit score is important for individuals and businesses to differentiate between each other. Whereas credit ratings are investors’ tools for determining risky issues in institutions, credit scores are personalized tools used by individuals to borrow money confidently. Through active management and improvement of these metrics, the financial opportunities available are enhanced, and a brighter future is made possible.

{kind=link}